So you still don’t buy travel insurance. But you do

have car insurance, home insurance, and health insurance. Have any of these

netted you a payout large enough to cover all the premiums you’ve paid

throughout the years? Probably not. But you still have insurance—just in case.

So you still don’t buy travel insurance. But you do

have car insurance, home insurance, and health insurance. Have any of these

netted you a payout large enough to cover all the premiums you’ve paid

throughout the years? Probably not. But you still have insurance—just in case.

Unexpected

illness in Nepal

We recently returned from a trip to India and Nepal.

After two marvelous weeks exploring wildlife parks, temples, countryside, and

much more in India, we headed to Nepal. That was about the time my husband

Larry started feeling bad. A hotel doctor diagnosed him with bronchitis, gave

him medicine, and suggested he rest for a couple of days. We canceled our trip

to Chitwan National Park and stayed in Kathmandu two extra nights before flying

to Pokhara.

The night before leaving Pokhara, things started

going really downhill for him. He was admitted to the local clinic which

determined he needed to be at a better equipped facility in Kathmandu, where he

was taken by helicopter the next morning.

Without going into specifics, suffice it to say he

was in the hospital for eight days receiving treatment before he was cleared to

fly back to the States. Even though the cost for medical care in Nepal is

significantly less than equivalent services in the U.S., it doesn’t take long

in a hospital to incur a large bill.

Most U.S. insurance companies (especially if you’re

on Medicare or Medicare advantage-type program) won’t guarantee payment to a

hospital in a remote location like Nepal, which means we had to pay our bills

(make sure your credit card limit is fairly high) and then file claims for

reimbursement.

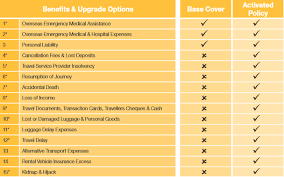

|

| Add caption |

Weather

event in Antarctica

That was the second time we had a large claim during

travel. About two years ago we went to Antarctica with an extension to Easter

Island following the icy expedition. Weather created the problem this time as

we could not get back to mainland Chile when scheduled, which played

havoc with our flights to Easter Island and later return to the U.S. In all we paid

out nearly $7000 more to continue our journey and return home afterwards, which the insurance company covered in full. Yes, travel insurance cost can be hefty, but we would never have gone without

it because of the uncertainty of traveling in remote parts of the world.

Before each trip, check the credit card on which you

book travel (cruises, flights, tours, hotels, etc.) to see what kind of

coverage is offered for non-refundable expenditures as well as medical expenses.

If it’s substantial, you may be able to lower the amount of coverage purchased

for regular travel insurance. You can consider a med-evac type of policy, too,

although most regular travel insurance policies include around $150,000 for

that service (which is highly unlikely to be used and does not guarantee

transport back to the U.S. only to the nearest facility that can provide

necessary treatment).

Even if your destination isn’t so far away as

Antarctica or Nepal, travel insurance is a good investment. Many costs are

incurred prior to travel, and things can disrupt your plans (luggage didn't arrive where you did? Flights delayed or cancelled?) even before a trip

as well as during. I would never book a major trip without insurance—just in

case.Photos from free sources

No comments:

Post a Comment